Non vbv bins If you’ve spent any time researching online payment systems particularly in high-risk transaction environments you’ve probably come across the term “Non VBV BINs.” Despite being widely discussed across forums, blogs, carding communities, and payment-related Reddit threads, many beginners still don’t fully understand what the term actually means. This guide is designed to clear up the confusion once and for all, using simple language and real-world context.

Looking for non vbv bins? vist nonvbvshop.netIntroduction: Why This Topic Still Matters in 2026

You might wonder why anyone is still talking about “Non VBV” when Verified by Visa (VBV) was introduced back in the early 2000s. The answer lies in how slowly payment terminology fades from certain corners of the internet. Many e-commerce merchants, fraud prevention analysts, and even payment processors still reference BIN databases that classify cards as VBV or Non VBV. Additionally, in high-risk industries such as adult entertainment, online gambling, digital currency exchanges, and subscription billing, understanding BIN behavior can directly affect whether a transaction is approved or declined.

This guide will walk you through everything from the basics of BINs to the modern reality of 3D Secure 2.0 while debunking myths that continue to circulate in 2026.

Chapter 1: What Exactly Is a BIN? (Deep Dive)

1.1 The Basics

BIN stands for Bank Identification Number. It is the first 6 to 8 digits of any credit card, debit card, or prepaid card. For example, if a card starts with 414720, those six digits form the BIN. Every card issued globally has a unique BIN that acts like a postal code for the banking system.

1.2 What Information Does a BIN Reveal?

When you run a BIN through a lookup tool, you can typically see:

Category Examples

Card Network Visa, Mastercard, American Express, Discover, UnionPay

Issuing Bank Chase, Barclays, Sberbank, Nubank

Card Level Classic, Gold, Platinum, Signature, Infinite

Card Type Credit, Debit, Prepaid, Commercial, Corporate

Country of Issuance US, UK, BR, IN, DE, etc.

Contactless Support Yes / No

1.3 How BINs Are Used in Payment Processing

Every time you enter your card online, the merchant’s payment gateway looks up the BIN to decide:

· Which payment routing to use

· Whether to request 3D Secure authentication

· If the transaction falls under specific regional rules (e.g., EU’s Strong Customer Authentication)

· Whether to apply higher fraud scoring

BIN databases are updated constantly. In 2026, there are over 300,000 active BINs worldwide, with new ones added weekly as banks issue new card series.

Chapter 2: Verified by Visa (VBV) — A Complete History

2.1 The Origins of VBV

Verified by Visa launched in the early 2000s as a response to rising online fraud. Before VBV, a merchant only needed the card number, expiration date, and CVV to charge a card. Fraudsters loved this. VBV added an extra step: the cardholder had to enter a password or a one-time code sent via SMS.

2.2 How VBV Worked (Technical Overview)

When a card was enrolled in VBV, the issuing bank would redirect the customer to their own authentication page during checkout. The customer would then:

- Enter a pre-registered password, or

- Receive a code via text message or email

Only after successful verification would the bank approve the transaction. Merchants who supported VBV received liability protection if a fraudulent transaction passed VBV, the bank (not the merchant) absorbed the loss.

2.3 Why VBV Became Controversial

Despite its security benefits, VBV was widely hated by customers and merchants alike. Common complaints included:

· Password fatigue — Users forgot their VBV passwords constantly.

· Redirect loops — Customers got stuck on broken bank pages.

· Abandoned carts — Adding an extra step killed conversion rates.

· International friction — Non-local cards often failed VBV entirely.

This last point is where the term Non VBV BIN gained traction. Merchants noticed that cards from certain countries or certain banks would simply never trigger the VBV popup. Those transactions would go through as “non-authenticated” faster, but riskier.

Chapter 3: Non VBV BINs — The Real Meaning

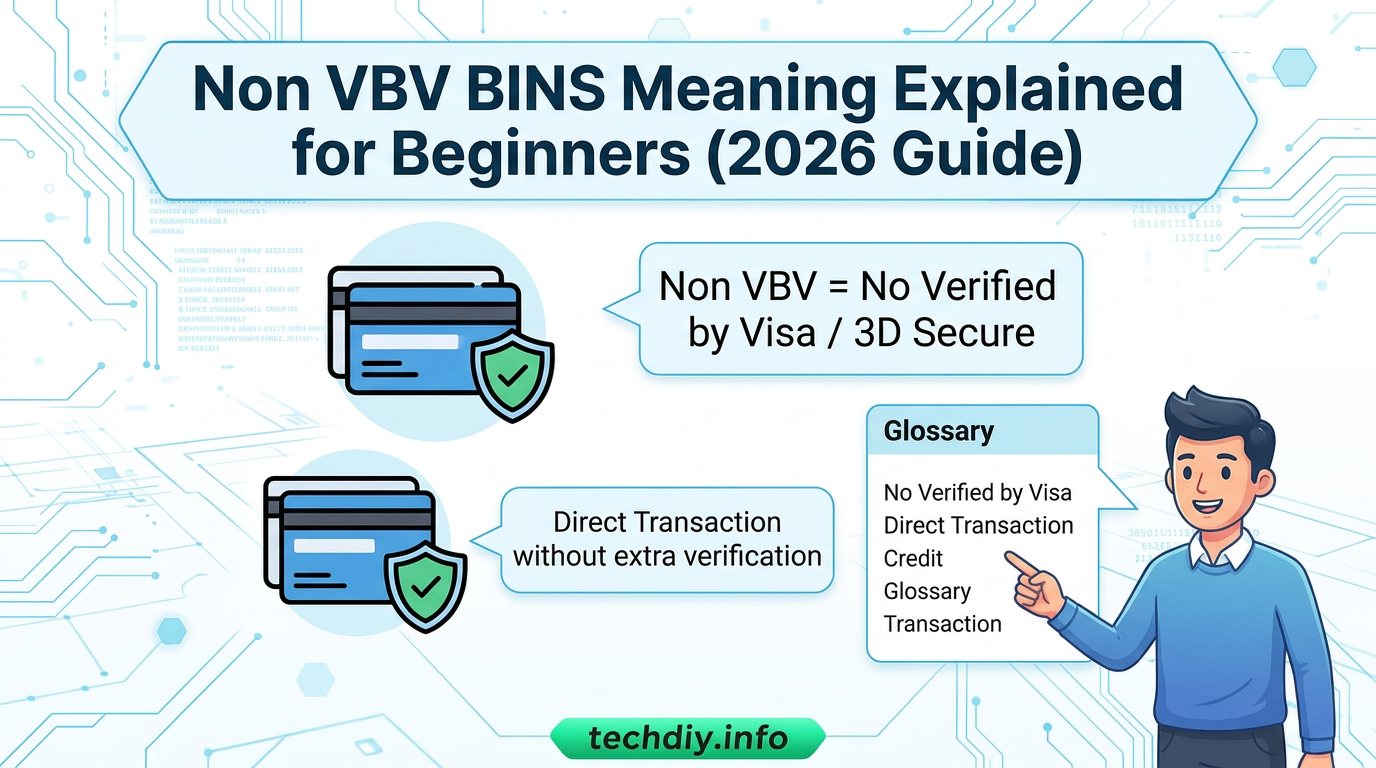

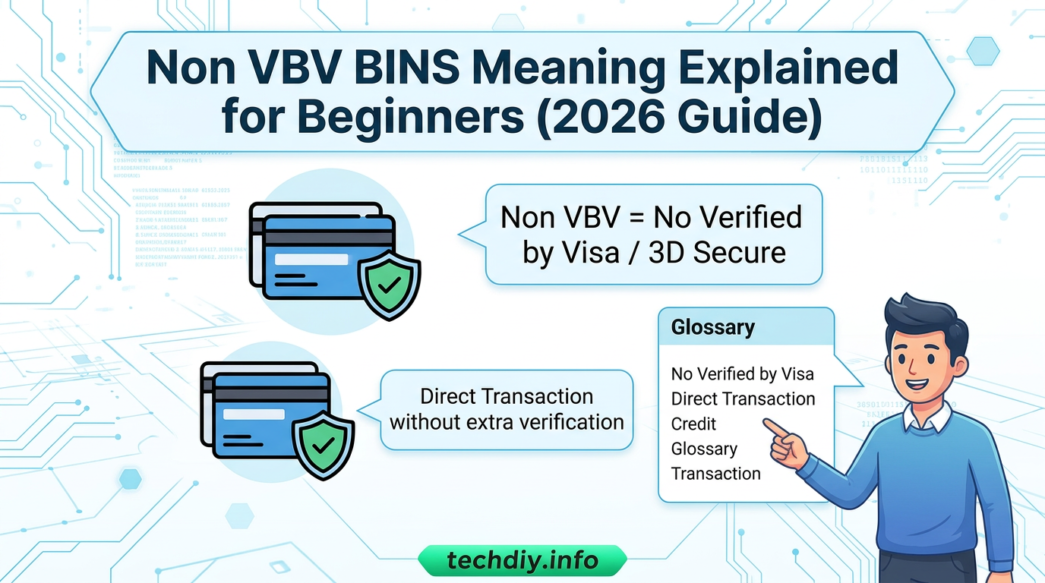

3.1 The Simple Definition

A Non VBV BIN refers to any Bank Identification Number linked to cards that either:

· Were never enrolled in the Verified by Visa program, or

· Do not trigger the VBV authentication challenge during checkout

However and this is critical the term has no official status. Visa never published an official “Non VBV BIN list.” The term emerged from underground forums and e-commerce communities as shorthand for “cards that tend to skip extra authentication.”

3.2 What Non VBV Does NOT Mean

Let’s clear up the most dangerous misconceptions:

Misconception Reality

Non VBV = guaranteed approval False. Issuers can still decline for insufficient funds, velocity checks, or fraud flags.

Non VBV = invisible to banks False. Every transaction leaves a digital trail.

Non VBV = works on every site False. Many merchants now use 3D Secure 2.0, which overrides legacy VBV settings.

Non VBV = always faster Not anymore. Modern risk engines may add invisible delays.

3.3 Why Non VBV BINs Are Often Called “High-Risk”

- Fraud exposure Without VBV, merchants have less liability protection.

- Chargeback vulnerability A cardholder can claim “not me” more easily if no authentication occurred.

- Geographic correlation Many Non VBV BINs come from countries with weaker fraud detection infrastructure.

- Industry focus High-risk sectors (gambling, crypto, adult content) actively seek Non VBV BINs to reduce checkout friction.

Payment processors often charge higher fees for transactions using Non VBV BINs specifically because of this elevated risk profile.

Chapter 4: Real-World Examples of Non VBV BINs (2026 Data)

4.1 Geographic Hotspots

As of 2026, cards from the following countries are more likely to behave as “Non VBV” in practice:

· United States — Surprisingly, many US-issued Visa cards still do not enforce VBV or 3D Secure, unlike Europe.

· Brazil — Local cards often bypass additional authentication due to domestic payment rules.

· India — Some older debit card BINs from public sector banks remain non-enrolled.

· Vietnam & Philippines — Many prepaid and debit cards lack 3D Secure support entirely.

· Russia — Due to sanctions and payment system isolation, Russian-issued cards often behave unpredictably.

4.2 Example BINs (Educational Use Only)

The following are anonymized examples for learning purposes (do not attempt to use them fraudulently):

BIN Prefix Issuing Bank Country Typical Behavior

414720 Chase USA Often Non VBV for low-value transactions

546357 Banco do Brasil Brazil Rarely triggers 3DS

401795 SBI India Older debit series — Non VBV

521234 TPBank Vietnam No VBV support

Keep in mind: Banks change their authentication policies frequently. A BIN that is Non VBV today may become 3DS enforced tomorrow.

Chapter 5: Modern 3D Secure — The VBV Replacement

5.1 What Is 3D Secure 2.0?

In 2026, the original VBV has been almost entirely replaced by 3D Secure 2.0 (3DS2). This is a completely different technology. Instead of a clunky password popup, 3DS2 uses:

· Risk-based authentication — Low-risk transactions (e.g., a $10 Amazon purchase from a known device) skip verification entirely.

· Biometrics — Fingerprint or face scan on a mobile banking app.

· One-time passcodes — Sent via SMS or email only when risk is medium.

· In-app approval — Push notifications directly from the bank’s app.

5.2 How 3DS2 Makes “Non VBV” Obsolete

With 3DS2, the concept of a card being “enrolled in VBV” no longer applies. Instead, each transaction is scored in real time. A card that used to be Non VBV might still trigger 3DS2 if:

· The transaction amount is high

· The device fingerprint is new

· The merchant is flagged as high-risk

· The customer’s location differs from the card’s country

Conversely, a card enrolled in 3DS2 might still process without any popup if the risk score is low. This is called a frictionless flow.

5.3 Why the Term “Non VBV” Refuses to Die

Even in 2026, the term survives because:

· Older BIN lookup APIs still return a “VBV Status” field (Yes/No/Unknown)

· Carding forums prefer legacy terminology

· Many merchants use outdated fraud filters that reference VBV

· SEO traffic as you’ve noticed remains high for this keyword

Chapter 6: The Merchant’s Perspective High-Risk Non VBV BINs

6.1 Why Some Merchants Want Non VBV BINs

In legitimate high-risk industries (e.g., subscription billing for adult content), merchants sometimes prefer Non VBV BINs because:

· Lower friction = higher conversion rates

· Fewer false declines Overly aggressive 3DS blocks good customers

· Recurring billing Some VBV cards require re-authentication for each charge, causing churn

However, this comes with a trade-off: higher chargeback risk. Many merchants use a hybrid approach: accept Non VBV BINs but add their own fraud checks (IP geolocation, velocity limits, device fingerprinting).

6.2 Payment Processor Policies (2026)

Major processors like Stripe, Adyen, and Square now handle 3DS2 automatically. As a merchant, you typically cannot “force” a Non VBV outcome. Instead, you can set rules like:

· “Require 3DS for all cards above $500”

· “Block transactions from BINs with high fraud history”

· “Allow frictionless for returning customers”

Some high-risk processors (e.g., CCBill, PayKings) still offer manual BIN filtering for Non VBV cards, but this is becoming rare.

Chapter 7: Common Myths — Busted for Beginners

Myth 1: You Can Buy a “Non VBV Card List” and It Will Work Forever

False. BINs change. Banks update their systems daily. Any list you buy online is likely outdated or a scam.

Myth 2: Non VBV Means No Fraud Protection

False. It only means no VBV. Modern banks use machine learning to flag suspicious transactions regardless of 3DS status.

Myth 3: All Prepaid Cards Are Non VBV

False. Many prepaid cards (e.g., Revolut, PayPal Prepaid) are fully 3DS2-compliant in 2026.

Myth 4: Non VBV BINs Are Illegal to Discuss

False. The term itself is neutral. However, using someone else’s card without permission is illegal everywhere. This guide is for educational and legitimate e-commerce understanding only.

Chapter 8: How to Check a BIN for Non VBV Status (Legitimate Use)

If you are a merchant or security researcher, you can check BIN information through:

- Free BIN lookup tools: BinList.net, binbase.io (limited accuracy)

- Paid BIN databases BINBase Pro, WhoisBIN (monthly updates)

- Your payment gateway’s BIN reporting Stripe Radar, Braintree Fraud Tools

- Test transactions Run $1 authorization with your own card to observe behavior

Warning: Do not use stolen cards or unauthorized test transactions. That is fraud.

Chapter 9: The Future — What “Non VBV” Will Mean in 2030

Looking ahead, the term “Non VBV” will likely disappear entirely. Here’s why:

· 3DS 2.3 and beyond — Upcoming versions will make all cards behave the same way: frictionless for low risk, challenged for high risk.

· Biometric passkeys — Apple Pay, Google Pay, and bank apps will replace passwords completely.

· Real-time BIN updates — Modern systems will check authentication capability live, not from a static database.

· Global regulatory pressure — PSD2 in Europe already mandates strong authentication; other regions are following.

By 2028-2030, “Non VBV BIN” will be about as relevant as “Non dial-up internet modem.”

Chapter 10: Frequently Asked Questions (FAQ)

Q1: Can a Non VBV card still be declined?

Absolutely. Declines happen for many reasons: insufficient funds, incorrect CVV, expired date, velocity limits, IP mismatches, or issuer-side fraud blocks.

Q2: Are Non VBV BINs only for Visa cards?

Originally yes VBV is Visa-specific. But the term is now used loosely for any card (Mastercard, Amex, Discover) that bypasses 3D Secure authentication.

Q3: How do I know if my own card is Non VBV?

Try making a small online purchase at a merchant known to use 3DS (e.g., Adobe, PlayStation Store). If you never see a verification popup or SMS code, your card may behave as Non VBV.

Q4: Why do carding forums love Non VBV BINs?

Because fraudsters want to avoid additional verification steps. Discussing this is not an endorsement — it’s an explanation of why the term persists.

Q5: Can a merchant block Non VBV BINs?

Yes. Many high-security merchants (SaaS, hosting providers, digital goods) set fraud rules to decline any transaction that doesn’t complete 3DS.

Q6: Is it legal to sell Non VBV BIN lists?

Selling publicly available BIN data (the first 6–8 digits) is legal. Selling full card numbers, expiration dates, or CVVs is illegal in most countries.

Final Thoughts: What Beginners Should Remember

If you take away only five things from this 3000-word guide, let them be these:

- A Non VBV BIN identifies a card that historically bypasses Verified by Visa — but that doesn’t mean it bypasses all security.

- The term is outdated Modern 3D Secure 2.0 has replaced VBV, but the old phrase lingers online.

- High-risk merchants sometimes seek Non VBV BINs for lower friction, but they accept higher chargeback risk.

- Never trust paid “Non VBV lists” Most are scams or dangerously outdated.

- Authentication is dynamic The same card may act differently on different websites, at different amounts, or on different days.

Understanding Non VBV BINs gives you a window into the history of online payments and the ongoing tug-of-war between security and convenience. As a beginner in 2026, your best move is to focus on modern 3D Secure concepts rather than chasing an obsolete label. Stay informed, stay legal, and always question outdated forum “wisdom.”